The short answer is no, and yes.

Should we be worried that recent US bank failures spill over into the UK banking sector? No. The recent failures have highlighted that although the US banking regulators have significantly tightened regulation around large systemic banks, the likes of JP Morgan, they have left a significant gap in the regulation and stress testing of smaller regional banks. A small bank in the US is one with less than £100bn in assets. The UK banking market doesn’t have this issue. Regulators around the world will be looking at their stress testing models but the UK will not have the same problem of loosely regulated smaller banks having made bad decisions. The failure of these smaller banks in the US has meant that wealthy and corporate clients have been moving their balances to larger banks, causing good old-fashioned bank runs. If you are a corporate treasurer in the US it is simply not worth the risk of holding large balances at smaller banks, hence we are seeing the domino effect.

So while we shouldn’t be worried about contagion reaching the UK, the “yes” is that we should be a little bit worried about the overall impact this could have on credit tightening.

Banks around the world are moving into “risk off” mode. This means banks will be looking to reduce their liquidity and interest rate risk.

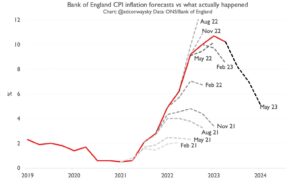

Credit tightening happens in a few ways. Central banks increase interest rates, thus de facto reducing the availability of credit by making it more expensive. N.B. regular readers will have noted that I have long been cynical of BoE inflation forecasts and predicting that we have not yet seen the end of interest rate rises the below graph shows how wrong BoE forecasts have been for the last 2 years.

N.B. regular readers will have noted that I have long been cynical of BoE inflation forecasts and predicting that we have not yet seen the end of interest rate rises the below graph shows how wrong BoE forecasts have been for the last 2 years.

However, credit availability is also driven by the risk appetite of banks and this can have an even greater impact on businesses and the economy.

This manifests itself in a reduction of available products, increased lending criteria, reduced individual criteria, and increased interest rate differentials.

For example, having a B credit rating may currently allow you to access £100k of financing at rates 5% above the base rate. As banks tighten credit it could mean in the future you only have access to £50k at rates 7% above base.

In a potential future credit-tightening scenario, it is vital that your business has a good credit rating. It is also vital that you look at possible ways to improve your score. Even if you aren’t seeing any immediate impact, if the economy worsens or your business faces issues in the future, improving your credit score now could make the difference between survival or failure. It could also save you thousands in future interest expenses.

One of the easiest ways to reduce future credit tightening risk is to understand what drives your credit score. We have partnered with Capitalise, who are backed by Experian, to help you do this.

You can log in to Capitalise here to find out more.

If you subscribe to their premium service, you can track and monitor the credit score of your customers and suppliers and also have a reduced, “no improvement no fee” access to their Experian-backed credit score improvement process. You may already be doing this with another credit checking company, however, we believe Capitalise have a stronger product.

Written by Gus Williams, Chief Executive Officer here at Bevan Buckland LLP